Oil is currently at around $120; in 2022 and 2014 it topped $100. If the barrel cost doesn’t decrease then it will continue to rise, but (my understanding of it is)…

Part of the reason fuel rises so quickly (but doesn’t drop as fast) when oil purchased at a spiked rate doesn’t flow into consumer tanks for a month or two is to essentially amortise P&L over a period of time.

Pump prices spike sharply to make more now, expecting to make less later, but they don’t initially rise to a point which represents parity with target margins at that higher purchase price. There’s an anticipation/hope that prices drop again, which factors into why there’s often a sharp rise at the pumps followed by a trickling increase of pence per week in some instances.

Another consideration for this, is that there’s only so much price pressure that consumer demand can withstand, and it’s often (across many markets) considered better to have a medium to hard hit to prices early, than a potentially larger one later or lots of smaller, but not insignificant rises.

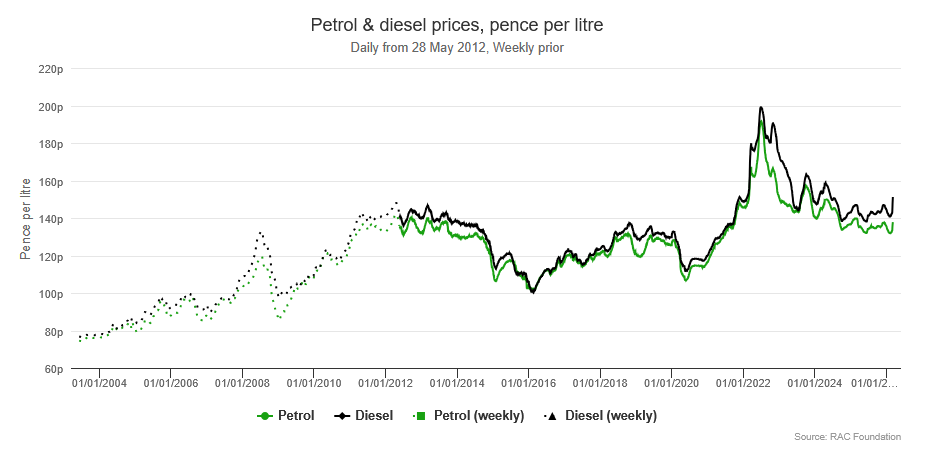

As evidenced here:

Other examples would be that a weekly bus ticket and increased travel times becomes more appealing and people significantly reduce their for-leisure driving. Wholesalers and retailers still need to shift the stuff, and there’s breakpoint where too few sales are made for an increased margin to cover operating costs. (Though I think that breakpoint is less of a concern in modern times, there is still an impact to the calculation from people reducing usage).

PlayStation have just massively bumped prices, and there’s speculation that part of the reason is to insure against further increases later - big jump early and take the PR hit in one shot instead of generating a regular bad news cycle of constant inflation. The other speculation is in preparation for GTA6, but…

Other factors for fuel in the short term are wholesaler and retailer demand attempting to front-load early on the open market to avoid only getting the highest rate after everyone else has battled it out. Then long term supply (and those later, trickle increases) is further impacted if production or release of reserves doesn’t pick up slack.

Circling back to my comment about prices not dropping as rapidly, as well a kind of “making the margins last” element, this delayed reduction can also be driven by lower-volume retailers having tanks full of the expensivo stuff; so while anyone who’s bought considerably cheaper doesn’t have to keep prices as high (assuming they aren’t covering losses from) they also don’t have to drop too much to become more competitive and attract customers. But also, they may have some losses or reduced margin average to rectify.